On Using EMTA Tax Data

On Using EMTA Tax Data

Or how did we get from insider trading to vanishing 100M€?

Housekeeping

We’re afraid this is another unplanned publication. The below text explains Twitter thread that started from something else and took an unexpected turn. It’s branching into multiple trees and contains several interesting points that, we strongly feel, require additional explanation.

And it’s important. It’s like of 100M€ importance.

None of the below discussion of Funderbeam Marketplace Rules is legal advice, we’re only describing our understanding of it. Neither are we familiar with Singaporean laws under which the marketplace operates.

Prologue

A while ago we learned that people could be using data from tax declarations that is published by Estonian Tax and Customs Board (EMTA) to take positions before the official monthly/quarterly reports are out on Funderbeam. It wasn’t immediately clear whether this info can or cannot be used, whether it’s insider trading or not.

Don’t get overly excited, in our opinion - it’s not. It’s too delicate topic to build tension with.

We did some investigation (before publishing any dubious claims) - read Funderbeam Marketplace Rules and our conclusion (which might well differ from anybody else’ conclusion) was that tax data is public, generally available information, so no wrongdoing here even if this data is used for trading.

The part regarding Xolo was pretty strong statement, so we’ll make a quick diversion to explain our thoughts here.

Diversion - Xolo

We concluded that using tax declarations data is fine, but the specific wording reminded us of another case of asymmetric info - Xolo publishes last round (that was raised outside Funderbeam) valuation only to shareholders. We’ve drawn your attention to that several times and even suggested a workaround:

But according to Funderbeam Marketplace Rules - Xolo is probably not doing anything wrong (we can’t confirm this - company disclosures are described in Annex II, which has a bit milder choice of words).

Instead the people who use the info that is not public and not generally available (but could have material effect on price if it were) for trading, are likely not acting according to guidelines. Kind of counterintuitive, but now you know.

It’s similar to the case where certain Estonian bank’s stock brokers found a way to access companies’ stock exchange announcements ahead of publication (and very successfully bet on earnings releases). They weren’t guilty of obtaining the info, they were accused of trading based on it.

Guess same applies here - you can have the info, but you shouldn’t trade based on it.

But this is a diversion, not the main topic.

Act I - Belief Water

This is happening around July 19th - we’re following Belief Water closely for a couple of days already because there’s some heavy activity we cannot relate to anything (previous Teatmik link to Belief was not random). The Q2 report is due, but is not yet published.

Finally on 20th of July comes the announcement that Belief Water plans to publish Q2 report the next day at which point we tweet1:

By this time, we’ve done some homework and compared several companies’ multiple quarters’ reports to the data Tax Board publishes and found they’re definitely not 1:1 - so we add the disclaimer about giving only direction and possible explanation.

But turns out we’re wrong and it’s important to read on if you’ve gotten this far.

Firstly Madis Müür notifies us in private that Tax Board data lags one month (VAT declarations are due by 20th of next month, so the data is published sometime after that) and thus publications like Teatmik have quarters that are Dec-Jan-Feb, not the usual Jan-Feb-Mar. This becomes our working theory for the mismatch for a brief moment.

But then comes the main blow from Olavi Ottenson:

This is followed by lengthy private discussion with Olavi where he tries to explain and we try to understand the concept of reverse charge. We kinda-sorta understand it, but choose not to start explaining it to the readers - we think there are better and more authoritative sources for it, so we just release the following statements in the main thread (we have no idea whether the branching threads and the replies there are ever seen by our readers):

The topic concludes here, at least for the time being. While reading random article from Äripäev, we write in our notebook: “Äripäev regularly quotes tax data”. It crosses our mind that they could be wrong too, but well, Nugis is anonymous internet persona and they are biggest financial newspaper in Estonia.

The important takeaway for us is - don’t use tax declarations data to predict actual revenue.

Act II - Bolt

This is until Geenius publishes the following article: https://ari.geenius.ee/rubriik/uudis/kuhu-kadus-100-miljonit-bolti-varske-aruanne-keeras-varasema-teadmise-pea-peale/

We’re not paying subscribers either, so we just read the lead. Honestly, we didn’t yet connect the dots here (can’t go everywhere in depth), we just thought there’s likely a valid reason and it’ll surface sooner or later.

This is where we hear from Olavi again (always glad to hear from him - even if he points out our inconsistencies):

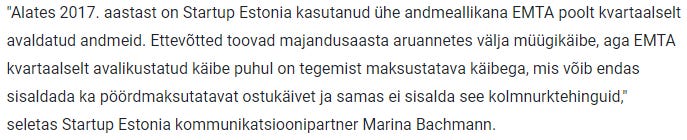

We hope we can provide this excerpt to our readers as it’s a quote from Startup Estonia and not Delfi’s intellectual property:

Well, well. So Nugis was not the only one to step into that same trap. The professionals from (not cheap) subscription newspapers and government programs do it too. Why we’re saying newspapers - because of course they were after scandal and clicks. They could do their research, ask for clarifications before publishing the article.

They deliberately chose not to.

Nah, this is not even schadenfreude, although we think we handled very similar situation way more cautiously.

The sad part is - at this point the damage to Bolt is done. There was a lot of hate in the comments towards Bolt and the startup scene in general.

And this is by no means the fault of Bolt, but the media that makes living on covering startups.

Act III - The Law

This part is added later (31.08.2021).

We always have subconscious itch to get to the bottom of things. This is one of the driving forces of Nugis.

So we wonder - if this is such a widespread problem - why isn’t it fixed yet? All the business media quotes the tax data all the time, yet it might well be that it’s NOT what it’s presented as. It’s even a bit funny (and sad) that Startup Estonia does it again while we’re at it:

EMTA info is presented as the ultimate truth of companies’ revenue, yet, on many cases, it definitely isn’t. It could be bloated by inside-EU purchases and it could be diminished by outside-EU sales.

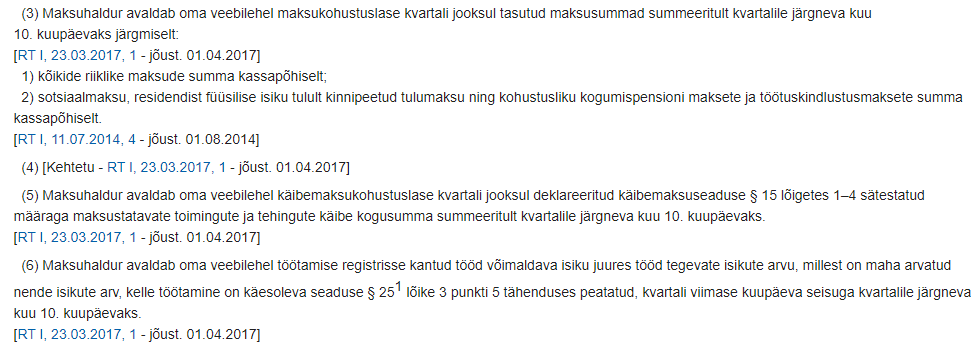

But what would it take to fix it? Not so easy, cowboy. Turns out what EMTA publishes is specified in the law:

Which law you ask?

To save you 30 seconds you’d spend looking that up:

So we gotta admit, it’s a dead end. Also fixing just reverse charges would be only partial fix anyway. This is probably a good place to give up.

Epilogue

If you think it was messy, then yes, it was. It started from (nonexistent) insider trading and ended up with scandal of the week on Estonian startup scene. But neither reality nor our thoughts are always linear.

We wrote it down here hoping it’s a little less messy and it won’t get lost forever in the depths of branching Twitter threads.

We’re still working on multiple standalone articles (stuff that tries to break new ground, not just explain Twitter ramblings), but there’re already now several other trains of thought we’ll need to clarify here in the future.

If you find these articles interesting, we can deliver them straight to your inbox:

Belief Water Q2 report was followed by their 5-year financial plan on July 26th which also included plans for IPO around 2026-2027 on Tallinn Stock Exchange. We go on to comment on this in yet another Twitter thread: