Price Discovery vs Valuation

Price Discovery vs Valuation

What is a good validation of company's value or why are there so called down rounds?

Intro

In our previous articles we’ve discussed in length terms like market value and fundamental value and also explored in-depth how to get from instrument price to market cap and how different instruments represent different parts of the company.

Today we try to think aloud about where the price comes from both during trading and fundraising campaigns. And also, why there’re up and down rounds.

Trading

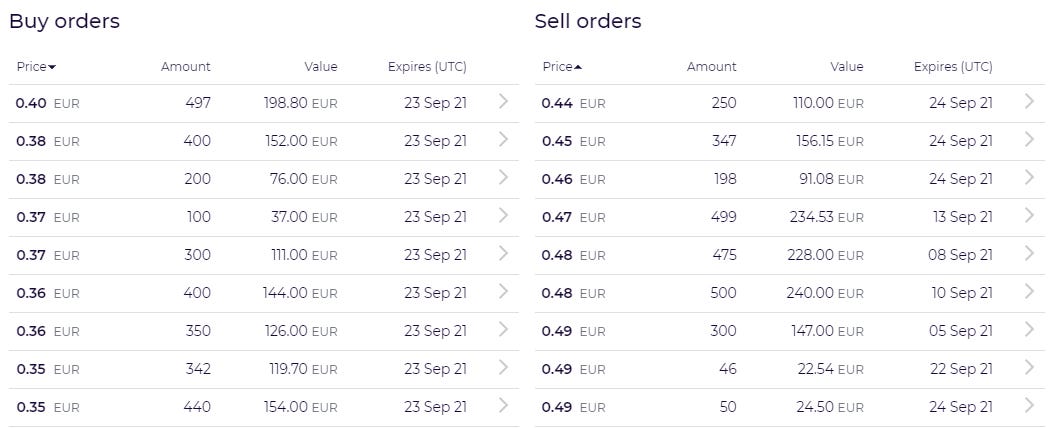

On the marketplace, there’re always two prices:

Bid or the amount that somebody is willing to pay for any instrument

Ask or the amount that somebody is willing to sell the instrument for

If you enter a buy order with the ask price, it gets filled and the last price becomes ask price, pushing the price up.

If you enter a sell order with the limit equal or below the highest bid, it’s also matched and last price becomes bid price, pushing the price down.

The difference between ask and bid is called spread and on low liquidity market like Funderbeam, the spreads can be pretty wide, especially for the sparsely traded instruments.

The market makers usually quote the price in both ways and pocket the spread. There isn’t much thought process involved here, you just keep the orders small. Should the price move down suddenly, you might be holding instruments that you bought higher, but if the price moves up, you gain from the holdings anyway.

On the above example, the spread is 4 cents which seems low, but is actually 10%. If the last price was 0,4, buying 1 token from ask will make the price go up 10% and vice versa1.

Add some buyers to the marketplace, some influencers who will say good things about the company and voila, the price starts moving upwards. But issue a report with flat numbers and there’s sell-side pressure.

This constant search for equilibrium between supply and demand is price discovery.

Skin in the Game

Have you ever tried to play poker for just chips? Like, without having any actual money (or at least clothes 😊) at stake?

If you have, you might know how people raise and call down every hand and the bluffs never work cause people don’t have absolutely anything at stake. Of course the same can happen if people play way under their limits - they play with money towards which they’re completely indifferent.

Poker is meaningless if you don’t have skin in the game. And when you have, you suddenly start thinking about chances of making your hand, don’t call down every hand and the bluffs might start working too.

Let’s try to put that into the context of investments.

Imagine a 1 unit trade - Funderbeam prices usually being below 10€ - you don’t really care if it moves anywhere. For example, we’ve bought 1 share unit if we’re holding loan notes just to know if there’re any shareholders votes and what’s being voted on. The sums might be €€.

Next - the people who make money by quoting the spread usually do it with less than 500€ at a time. As we concluded earlier, this more about acting fast than deep analytics. €€€ might be moved here just hoping to pocket the spread.

Then the swing trades - people might have ideas about where the price goes short term (for us short term is days and weeks, not minutes) and they bet on it. Maybe it’s quarterly results or a product launch or stock split. People are likely to bet meaningful money (€€€€) here and are familiar with the company and the business at the very least.

And then come the investments - likely to be in €€€€€ range, depending on portfolio sizes of course. This is where people actually think about company fundamentals, look at the annual reports, product-market fit, team, sales channels and so on and so forth. They have skin in the game.

So we argue that the amount of due diligence is a function of investment size.

Recently we brought out a situation where some people are trying to buy Funderbeam 1 instruments at twice the price what seems to be the general consensus and at 3x than the lowest priced instrument. But these are below 100€ trades and the buyers probably haven’t put much thought into it.

Time

Those small, €-€€€, trades happen quite often - in most of the cases daily, sometimes even hourly. They can change the value of the company considerably - in the example above, company value changed 10% just by buying or selling 1 token - yet this doesn’t have absolutely anything to do with this company’s financials. Siidrikoda regularly fluctuates 20-30% both ways without anything happening except low volume trading.

Add a couple of optimistic swing trades here and there into the mix, then good communication skills by the company, article or two in local business media which is concentrating more on market mechanics than actual business of the company - and you might have landed a winner.

Market cap soars, investors are happy, founders’ net worth is going through the roof. Nobody is paying attention if the price has any connection to the reality or not. Of course, from time to time someone takes a bit of profit, there’re corrections in price and then the party continues.

And it could continue if we were on a real stock market (where it often does), not Funderbeam.

Fundraising

So you’re sitting there, smiling at your fat multibagger of unrealized profit when suddenly the trading is halted and the company starts raising money.

Now the lead investor(s) begin doing their due diligence and suddenly the price that was OK to buy 50 shares at, is not good any more to buy 10 000 shares at.

The thesis “somebody buys it tomorrow for more” is replaced with a question: “does it make sense to invest at market cap 50x revenue?”. Might well turn out that it doesn’t and the company is valued well below what the market price was before the round.

Of course if you’re the one who bought at the top just before new fundraising started, you’re down and you’re angry. But in the grand scheme of things and long enough time span, there’re some good aspects to it:

If the company raises the current round at 50x revenue, then what’s the expectation for the next round? 50x might be fine in the very beginning (like, MRR below 10K but the IP looks promising), but maybe not for a 5y old company. Raising at too high valuation could make the next round trickier than necessary.

There’s expectation that at some point the P/S (or revenue multiple, whatever you prefer) comes down. For P/S to decrease, the company’s revenue has to either grow faster than price or the price has to come down. So the pressure to grow more might become unrealistic, and not meeting the expectations is probably worse than setting them lower in the first place.

If the company raised previous round at 10x revenue and is now raising at 30x revenue, one might ask what changed? It might well be that completely new markets opened up for the company and they’re raising money to seize the opportunity, but if the only reason for higher multiple is market price, then it raises a red flag.

Funderbeam Process

What you usually experience when investing is one of the two:

Constant large-volume supply and demand based price discovery on stock exchanges (including a lot of speculation). Think of NASDAQ or NYSE.

Extensively DD’d discrete funding rounds with months/years between by VCs and syndicates. Think of EstBan or AngelList.

But Funderbeam is hybrid of these two - during ordinary trading, supply and demand based price discovery takes place and forms the market cap.

And every once a while - whenever the companies run out of money and need to sell more shares, the whole process switches into model-based valuation mode (even if the “model” is just revenue multiples).

Sometimes there’re conflicts between the two, but obviously the companies need lead investors and their money, so model-based valuation takes priority.

This is also a kind of reality check for the market - there rarely are any good reasons to get your money in at conditions that are considerably worse than during campaign.

This process raises opportunities for trading as you can usually get clues from the reports about when the fundraises are about to start and can run your own valuation models. If the companies are undervalued, it’s time to buy and if overvalued, it’s time to sell and add more during fundraises.

To gain some edge, you need to know where you stand at all times, meaning you always need to compare model-based value to actual price.

You might have a question - why are we giving away our edge by writing this down instead of using it to make money? There’re several reasons:

Market inefficiencies always work both ways - today we might gain, tomorrow we might lose. We’ve made a couple of good calls (see below) and we’ve been in unfavorable positions because of the market participants are not always rational.

We’re long-time investors and we believe that the prices (should) rise and fall in unison with companies’ results. Instead, what we see is small, insignificant events amplifying the price movements in both directions (exaggerated by low liquidity).

Examples

Here’re a few examples or recent funding rounds.

Barking

At the top of the craze, Barking’s price was over 30M, putting the revenue multiple at around 100x. By the time fundraising started, the market cap had come down to 20M, but was still way too much for the lead investors.

In the end the premoney valuation was agreed at 9M (still firmly above their first Funderbeam round at 5,3M premoney). Surely cold shower for some, but we tend to agree that it was a sensible move from future rounds’ perspective.

We owned Barking since first campaign and sold most of our position before round 2, because the price had gotten way ahead of revenues. We added a bit from second round.

Despite everything, we think that Barking’s 3rd round will be easier than Promoty’s one.

Funderbeam

Funderbeam’s last campaign was also well below what the market had priced it:

Well, just days before campaign start, Change made the following statement:

If the market value goes from ~30M to 116M in a matter of 2 months based on 60K€ and 21K shares changing hands - does it mean we all have to pay that price now? That’s ~0,086% of the company, while during the campaign, a total of 6,65% was sold.

We’re not even discussing the fact that valuation was likely agreed well before the campaign start and that Change guys did some solo there seems like their own problem.

Funderbeam’s runway and other financials are reported regularly and it’s just a matter of doing your homework. We didn’t have stake in Funderbeam before and didn’t add during the campaign.

Upsteam

Upsteam is a different beast - they’re raising their 3rd round a bit above market value, but current 10,5M is still down from 13M premoney in their 2nd campaign. As their business and expansion plans didn’t go all that well during Covid time, so they had to trim their expectations a bit.

Our thought process regarding Upsteam went as follows:

Their business is cyclic - they earn way more during warm weather than in winter

Their runway was known and the 3rd round was never a secret

They surely worked their asses off to show the absolute best numbers they could before the campaign

At the time we started thinking about investing (more) in Upsteam, the loan notes were traded below 5M mcap and share units at ~30% premium. So we sold share units from 2nd round (at small loss) and put the same money into loan notes.

This is not just hindsight, we also said it before the campaign:

Change

It didn’t catch much public attention, but Change was valued around 320M at the top, but soon after raised money outside Funderbeam at 175M and is now valued at 140M. Quite a rollercoaster, but way less bad publicity than Barking 2 campaign. We’ve stayed out of Change so far.

By the way, Change’s CNG instrument regularly trades well below share unit in their own app, but is denoted in BTC. This opens up some interesting possibilities for arbitrage and moving from BTC to EUR (see the whole thread if interested):

Bikeep

Bikeep raised at market value, but the one aspect we forgot was that in first round, loan notes were issued and in second round they’ll most likely add share units. We discussed this issue and different pricing quite emotionally here (there’ll be a moment of truth soon, when share units start trading):

Upcoming rounds

Due diligence during fundraises works both ways - we’ve covered down rounds this far, but there’s always the potential to have up rounds.

Recently we noticed that Nudist is hinting at new round - we’re pretty sure that would be an up round considering that the company has shown good results, but the price is still at first campaign level. They raised at 2,75M previously and can probably pull at least twice that in second round.2

Another potential candidate for up round is Costpocket, although their price has already gone up since we first wrote this (this article has been 1,5 months in the making). But being at breakeven surely adds optionality.

Subsequent Rounds

Wrapping up - here’s a list of things you should follow for your investments:

Runway - runway shows how many months are left until the company runs out of money. Profitable companies usually don’t report this, but sometimes still raise money to cover big one-time expenses (like Ampler raising money for new factory).

Breakeven/profitable - in theory, you might not need to raise money ever again if you’re profitable. These companies might trade at elevated multiples just because now might well be the best entry point there is.

Revenue multiples (P/S) - follow the revenue number and make sure revenue growth doesn’t get too much behind price growth.

Revenue growth - faster growing revenue justifies higher multiples, but it still has to make sense.

Conclusion

Funderbeam has a hybrid approach where during trading supply and demand based price discovery is used, but every once in a while - during fundraises - this switches to model based valuation. We think it’s a good thing that the market doesn’t go completely unchecked for extended periods of time.

In order to be successful, you constantly need to know where the market price stands in relation to models, especially when the companies’ runways get shorter. This way you won’t get caught off guard with down rounds and on the other hand, you might sometimes find undervalued gems.

All this contributes to general market efficiency, which we believe is in the interests of all market participants.

Housekeeping

If you don’t bother to follow our everyday ramblings on Twitter (https://twitter.com/NugisAino) where we also announce the new articles, you might want these longer articles delivered to your email:

Considering Funderbeam is taking 0,5% fee on sales, it’s more profitable to trade the instruments which spread is the widest.

Note added 16.09.2021 - please be aware that Nudist currently has loan notes and is likely to emit share units next, which, even if there’s no real reason, could put loan note holders into unfavorable position (as we’ve seen with multiple other cases, namely Upsteam, to lesser degree Ampler and the next candidate is Bikeep, although the share units don’t trade yet).